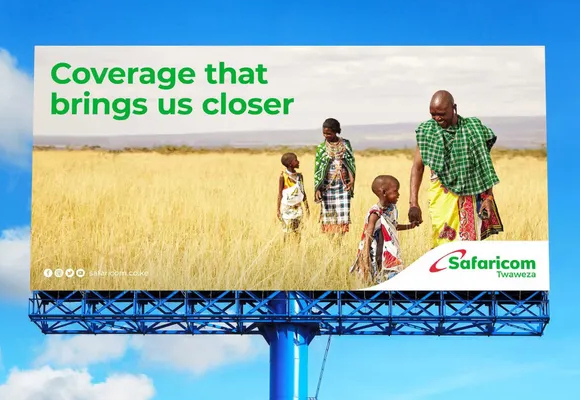

Kenya’s pension sector stakeholders have renewed calls for sweeping reforms to widen retirement savings coverage, strengthen compliance, and rebuild public confidence in pension systems.

Speaking during the Zamara 2025 Pension Convention in Mombasa themed “Disrupting for Impact: Transform, Integrate and Sustain”, the Chairperson of the National Assembly’s Finance and National Planning Committee, Kimani Kuria, said recent legislative amendments including the Tax Amendment Act 2024 and Finance Act 2025 have introduced incentives to encourage Kenyans to save for retirement.

However, Kuria, who is also the Molo MP, lamented that while formal sector workers enjoy structured schemes, nearly 80 per cent of Kenyans in the informal economy remain excluded, exposing millions to financial insecurity in old age.

“The pension industry must design flexible products that meet the needs of informal workers like boda boda riders, traders, and digital creators,” he said, urging prompt pension payments to build trust among savers.

Kuria lauded the Public Service Superannuation Scheme (PSSS) launched in 2022 for improving accountability through shared contributions between government and employees, ensuring retirees receive benefits faster. He revealed that automation has streamlined pension processing, enabling retirees to get their first payments within a month of leaving service.

To curb non-remittance of contributions, Kuria disclosed that amendments to the Public Finance Management Act have made it a criminal offence for accounting officers who fail to remit deductions a step meant to safeguard workers’ retirement funds.

Zamara Group Executive Director James Olubayi said the annual convention provides a platform for innovation and collaboration across the retirement ecosystem, focusing on how technology, governance, and data can strengthen pension systems.

Retirement Benefits Authority (RBA) CEO Charles Machira identified delayed remittances as the industry’s biggest threat, revealing that as of September, Ksh65 billion in pension contributions remained unremitted, mostly by public institutions and county governments.

“We have proposed legal changes to allow KRA to freeze accounts of employers who fail to remit pension deductions,” Machira said, adding that such negligence must attract personal liability.

Machira emphasized the need to expand voluntary savings and increase participation from informal sector workers, saying a stronger pension system will ease dependency and support financial stability for future generations.

{kind=link}

{kind=link}

online american casinos that accept paypal

References:

jobteck.com

casino sites that accept paypal

References:

https://didiaupdates.com/employer/best-paypal-casinos-2025-best-casinos-accepting-paypal/

These games load fast, accept crypto bets, and allow instant withdrawals, making them perfect for high-speed gambling.

BitStarz has developed its own line of exclusive games, all built for crypto gambling.

You can easily sort games by category, provider, or popularity,

ensuring you always find the perfect title to play. If

you’re looking for top-tier casino games, BitStarz has one of the best

selections in the industry. The longer you play,

the more games you unlock, and each week, a new game enters the rotation.

You’ll have 7 days to meet the 40x wagering, and the free spins drop in daily

batches after your first top-up. It’s split across your

first four deposits, which means you’ll get a nice little boost

each time you top up. You can rely on him to provide you with the knowledge you need to get more out of your online gambling experience.

BitStarz Casino is a real-money site that pays out in regular currencies like USD and EUR and cryptocurrencies.

References:

https://blackcoin.co/bestes-echtgeld-online-casinos-in-deutschland/

If you choose a market-focused portfolio, you’ll have to pay

a 0.30% advisory fee, which is higher than others on our

list. With Intuitive Investor, you can speak with a financial advisor when you need to at no additional cost,

and without needing a hefty minimum balance. If you want to align your long-term

savings goals with your investing portfolio, Betterment could be a viable option. We also like that you have the option to access a human advisor,

though this will increase your advisory fee. Otherwise, you’ll pay a relatively

low annual advisory fee of 0.25%, on balances of $24,000 to $1 million or with

$250+ monthly recurring deposit across eligible investments.

Whether you’re planning a weekend escape or a once-in-a-lifetime trip, Caesars makes it

easy to find the perfect Vegas hotel on the Strip for your vibe,

your style, and your moment. The majestic Caesars Palace on the Las Vegas Strip has a legacy as

a world-class destination for dining, gambling, shopping,

service, entertainment, and nightlife. From the prime location on the

Atlantic City boardwalk to the abundance of amenities and entertainment options, The

Caesars Atlantic City Hotel & Casino guarantees a memorable experience for families

and guests of all ages. For those looking for a fine dining experience, Morton’s The Steakhouse,

located near the main entrance of the hotel, is the perfect spot for a classic martini and steak dinner.

The upscale nature of the property is demonstrated not only by

the 135 table games and 2,000 slot machines in the casino, but also by the presence

of the Pier Shops at Caesars, home to high-end names like Gucci and Burberry.

Stardew Valley was made by a single guy, without

a game engine, you are using a game engine and it’s one

of the easiest in the world and you still need AI, Are

we deadass gang? I cannot stress this enough, everything you input into this

model will theoretically be able to show up in AI results giving everyone

access to YOUR games content. As a Roblox game dev with 9 years experience that manually codes my whole life until recently,

this is my take. The point isn’t about being too lazy

to make a game — it’s about radically accelerating Roblox game creation. To me,

this isn’t just about making money, it’s about making something

ridiculously affordable and accessible. This is not only incredible, it’s game changing.

References:

https://blackcoin.co/best-fast-payout-casinos-in-australia/

Der Willkommensbonus bei Jackbit besteht aus Freispielen und hat keine Umsatzbedingungen. Ja,

einige Online Casinos bieten Sofortauszahlungen ohne umfangreiche Anmeldeprozesse an. Dies macht die

Methode besonders attraktiv für diejenigen, die sofort spielen und ihre Gewinne schnell

abheben möchten.

Dank No-ID-Casinos können Spieler nun anonym von überall aus spielen. In keinem Casino mit KYC-Verfahren können Spieler spielen, ohne ihre Identität preiszugeben. Sie sind alle dezentralisiert und nicht nachverfolgbar, sodass Sie nach Belieben diskret spielen können.

Zu diesem Zeitpunkt können Sie Ihr Willkommensangebot

einlösen, wenn Sie einen Aktionscode haben, und um echtes Geld spielen. Wenn Sie sich für ein Casino entschieden haben, müssen Sie sich nun für ein Konto registrieren, um um echtes Geld spielen zu können. Sie sind daher perfekt für Spieler, die

gerne diskret spielen.

Ferner können Sie auch klassische Karten- und Tischspiele

wie Video-Poker, Blackjack, Roulette oder Baccarat nutzen. Nicht zu vergessen sind die 50 Freispiele, die Sie on Top für das Spiel “Wanted Dead or a Wild” bekommen können. Dabei gibt es einen Willkommensbonus mit einem

großzügigen Einzahlungsbonus von 200 % bis zu 1 BTC. Mega Dice Casino bietet eine große

Auswahl an Casino-Spielen, darunter klassische Karten- und Tischspiele und Live-Dealer-Spiele, und unterstützt auch mehrere Kryptowährungen für

Ein- und Auszahlungen.

References:

https://online-spielhallen.de/24-casino-erfahrungen-ein-umfassender-uberblick/

**memory lift**

memory lift is an innovative dietary formula designed to naturally nurture brain wellness and sharpen cognitive performance.